Ghana’s financial technology landscape has undergone a dramatic transformation over the past few years. Where once your only option was to walk into a bank and open a savings account earning negligible interest, today a wave of digital-first fintech platforms gives ordinary Ghanaians the ability to grow their money from their smartphones — often at rates that significantly outperform the traditional banking sector.

This article reviews the top fintech apps currently available in Ghana that allow you to accrue interest on your deposits, compares their rates, structures, and risks, and helps you decide which platform is best suited to your financial goals.

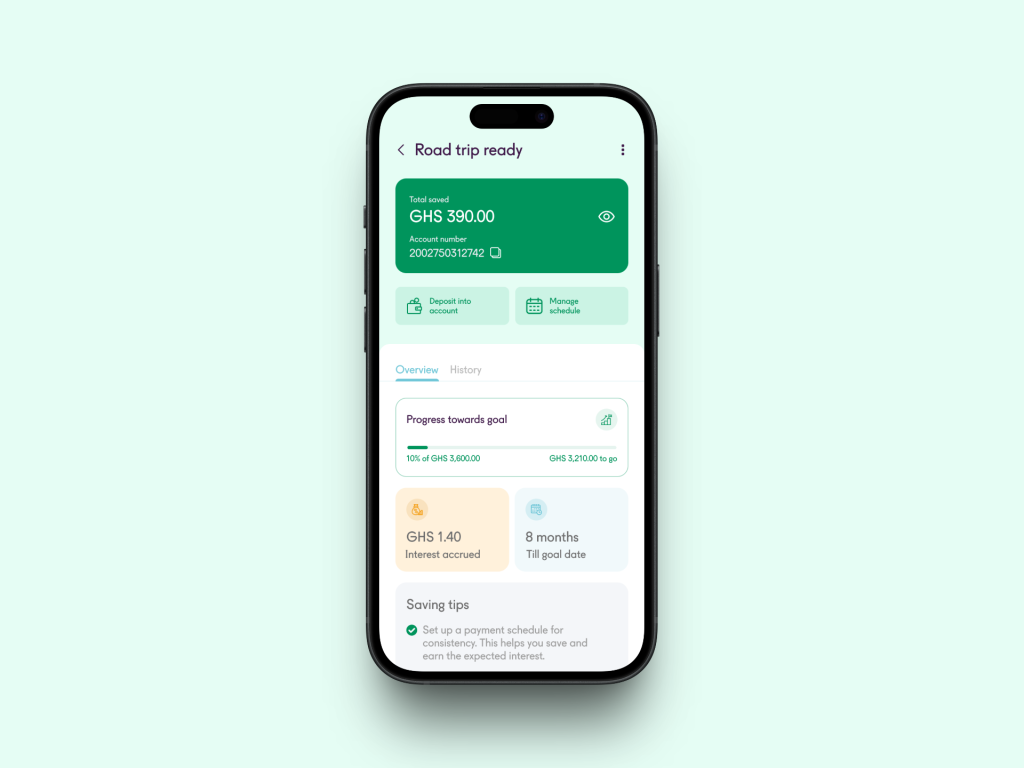

1. Affinity Africa — Best Overall for GHS Savers

Affinity Africa is a digital savings and loans company licensed by the Bank of Ghana. Unlike investment apps that route your money into mutual funds or foreign markets, Affinity operates like a fully regulated financial institution — which means your deposits carry the protection that Bank of Ghana licensing provides.

Products and Rates

- Daily Account: 3% p.a. — fully liquid, earn on every cedi, every day

- Growth Account: 5% p.a. — standard savings with slightly better returns

- Boost Account: Up to 11% p.a. — goal-based savings with fixed tenors

The Boost Account is Affinity’s flagship product and its most competitive offering. You set a savings target, choose a tenor, and commit to regular contributions. In return, you earn the highest available GHS rate on the platform.

Withdrawals beyond your free monthly quota can cost you the month’s interest, so it rewards disciplined savers.

Key Strengths

- Bank of Ghana licensed — strongest regulatory protection of any app reviewed

- No account fees or transaction charges

- Instant account setup with just a Ghana Card and mobile number

- Goal-based tools and spending dashboards included

Affinity is the most straightforward recommendation for any Ghanaian who wants to grow their savings in cedis with minimal complexity and maximum regulatory safety.

2. Achieve App — Best for Daily Compound Interest

Achieve is built by Petra Securities Limited, an SEC-licensed firm. Its core product, DigiSave, deposits your savings into the Plus Income Fund — a mutual fund managed by Black Star Advisors.

This means your money is actively invested, not simply held in a deposit account.

Products and Rates

- DigiSave (Plus Income Fund): Approximately 9% p.a. (market-linked, varies with T-bill rates)

- Interest accrues daily and compounds over time

- Minimum deposit: GHS 10

Because returns are tied to a mutual fund, Achieve is technically an investment product rather than a deposit. This means returns are not guaranteed — they follow the underlying fund’s performance, which is itself closely correlated with T-bill rates.

As T-bill rates have fallen sharply in 2025 and into 2026, Achieve’s returns have moderated accordingly.

Key Strengths

- Daily compounding maximises returns for long-term savers

- No lock-in period — standard withdrawals are free

- Multiple goal “buckets” to organise savings for different purposes

- Express withdrawals are available for a 1.2% fee

Achieve suits savers who want compound growth without locking funds away, and who are comfortable with modest performance fluctuations tied to the local money market.

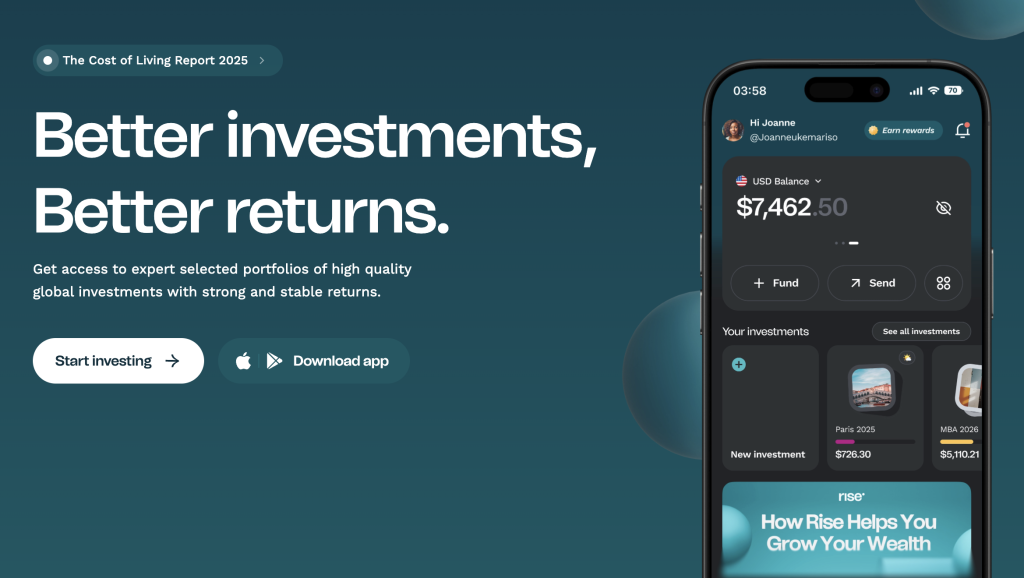

3. Risevest — Best for Protecting Against Cedi Depreciation

Risevest takes a fundamentally different approach from the other platforms on this list. Rather than growing your savings in cedis, it invests your money in dollar-denominated assets — US fixed income, US real estate (REITs), and US equities.

This means you are not just earning interest; you are also hedging against any future depreciation of the Ghanaian cedi.

Products and Rates

- Fixed Income (USD): ~10% p.a. — US bonds and fixed-income instruments

- Real Estate (USD): ~15% p.a. — US real estate investment trusts (REITs)

- Stocks (USD): ~14% p.a. historical returns — US equities

- Minimum deposit: $10

The real power of Risevest is the currency dimension. Even if you earn “only” 10% in dollar terms, you benefit additionally if the cedi weakens against the dollar over your investment period — a pattern that has historically played out over time. Conversely, if the cedi strengthens, your GHS-equivalent returns could shrink.

Key Strengths

- Dollar-denominated returns provide a natural inflation and currency hedge

- Three distinct risk tiers: stable (fixed income), moderate (real estate), growth (stocks)

- Goal-based saving plans available

- Returns among the highest in this comparison in absolute terms

Risevest is ideal for savers with a medium-to-long time horizon who want to preserve the purchasing power of their savings against currency risk, not just earn interest in cedis.

4. Bamboo — Best for Investing in Global Markets

Bamboo is a brokerage app rather than a savings platform. Its primary purpose is to give Ghanaians access to US stocks and ETFs — it does not offer a fixed interest savings product.

Returns come from capital appreciation and dividends on underlying equities, not from a guaranteed interest rate.

Products and Rates

- US Stocks and ETFs: Market-linked (no fixed rate)

- Fractional investing — buy a slice of any US stock

- Recently integrated with Affinity Africa for seamless GHS wallet funding

Bamboo belongs on this list because it is a legitimate and popular option for Ghanaians trying to grow long-term wealth. Over a 10-year horizon, diversified US equity exposure has historically delivered annualised returns in the 10–12% range. But there is no guarantee, and short-term volatility can be significant.

Key Strengths

- Access to globally diversified investments unavailable through local platforms

- Fractional shares make entry affordable

- Long-term wealth-building potential

Bamboo is best suited to patient, risk-tolerant investors with a long time horizon rather than those looking for predictable short-term interest income.

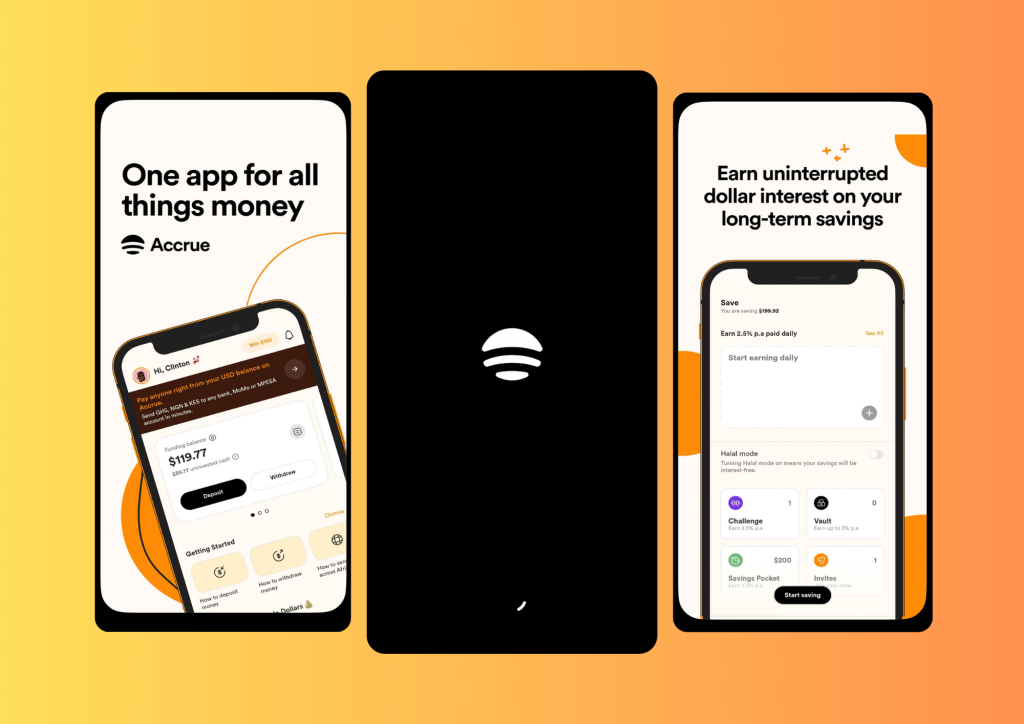

5. Accrue — Best for Multi-Asset Flexibility

Accrue allows users to invest across a range of asset classes — stocks, cryptocurrencies, and other instruments — from a single app. It caters to users who want flexibility and exposure to multiple markets simultaneously, and appeals particularly to younger, more tech-savvy investors.

Products and Rates

- Stocks: Market-linked returns

- Cryptocurrency: High-volatility, potentially high returns

- Low minimum investment threshold

Accrue carries the highest risk profile of all five platforms reviewed here, largely because of its cryptocurrency offering.

Crypto markets can deliver exceptional returns but can also lose significant value rapidly. It is not a savings product in the conventional sense — think of it as a speculative investment tool for the risk-tolerant.

Key Strengths

- Broadest asset class exposure of any platform reviewed

- User-friendly interface designed for beginners

- Two-factor authentication and security features

Accrue suits investors who want to explore alternative assets and are comfortable with the possibility of short-term losses in exchange for potentially higher long-term gains.

Side-by-Side Comparison

The table below summarises the key differences between all five platforms at a glance.

| Platform | Product | Rate (p.a.) | Currency | Type | Min. Deposit |

|---|---|---|---|---|---|

| Affinity Africa | Daily Account | 3% | GHS | Savings (liquid) | Any |

| Affinity Africa | Growth Account | 5% | GHS | Savings | Any |

| Affinity Africa | Boost Account | Up to 11% | GHS | Goal-based | Any |

| Achieve | DigiSave | ~9% (variable) | GHS | Mutual Fund | GHS 10 |

| Risevest | Fixed Income | ~10% | USD | Bonds | $10 |

| Risevest | Real Estate | ~15% | USD | REITs | $10 |

| Risevest | Stocks | ~14% (hist.) | USD | Equities | $10 |

| Bamboo | US Stocks/ETFs | Market-linked | USD | Equities | Small |

| Accrue | Multi-asset | Market-linked | GHS/USD | Stocks/Crypto | Small |

Note: T-bill benchmark rates as of March 2026 — 91-day: 4.71%, 182-day: 6.30%, 364-day: 9.34%. Inflation: 3.3% (Feb 2026).

Which App Is Right for You?

The “best” app depends entirely on your personal financial situation, risk tolerance, and time horizon. Here is a practical breakdown:

Choose Affinity Africa Boost if…

- You want to save in cedis with no foreign exchange risk

- You want the highest guaranteed GHS interest rate currently available (up to 11%)

- You value Bank of Ghana licensing and regulatory protection above all else

- You are saving towards a specific goal such as school fees, a car, or an emergency fund

Choose Achieve if…

- You want daily compounding interest without locking in your funds

- You are comfortable with modest performance variability tied to the local money market

- You want to save for multiple goals simultaneously in separate buckets

Choose Risevest if…

- You are concerned about long-term cedi depreciation eroding your savings

- You have a medium-to-long investment horizon (2 years or more)

- You want dollar-denominated returns and exposure to US financial markets

- You can tolerate exchange rate fluctuations in the short term

Choose Bamboo if…

- You want to build long-term wealth through global equity markets

- You are patient and comfortable with market cycles

- You are not looking for a fixed interest product but a growth investment

Choose Accrue if…

- You are comfortable with higher risk for potentially higher returns

- You want exposure to cryptocurrency alongside traditional assets

- You are an experienced investor looking for portfolio diversification

Disclaimer: This article is for informational purposes only and does not constitute financial advice.