The National Identification Authority (NIA) has moved swiftly to kill rumors that Ghana’s flagship biometric ID—the Ghana Card—can now be swiped, tapped, or scanned for everyday financial transactions.

In a worded statement released today, the agency called circulating media reports and social-media chatter “inaccurate and misleading,” emphasizing in no uncertain terms that the card “has not been activated for financial transaction purposes at this time.”

Although the Ghana Card has been pitched as having the capability of being linked to bank accounts or mobile-money wallets, the NIA’s statement has stated that the functionality has not been activated at this time.

“The Authority states unequivocally that the Ghana Card has not been activated for financial transaction purposes at this time,” the document reads. “Members of the public are advised to disregard any such claims and are encouraged to rely only on official communications from the National Identification Authority.”

Ongoing Negotiations

The NIA’s statement does acknowledge that serious conversations are happening behind closed doors.

“The National Identification Authority acknowledges that there are ongoing high-level discussions involving policy makers and key institutions within the financial and regulatory sectors regarding the potential future integration of the Ghana Card into financial transaction systems.”

These talks, the NIA notes, are part of broader efforts to “enhance digital identity usage and promote financial inclusion in Ghana.” But—and it’s a big but—“these deliberations remain inconclusive as of the time of this release.”

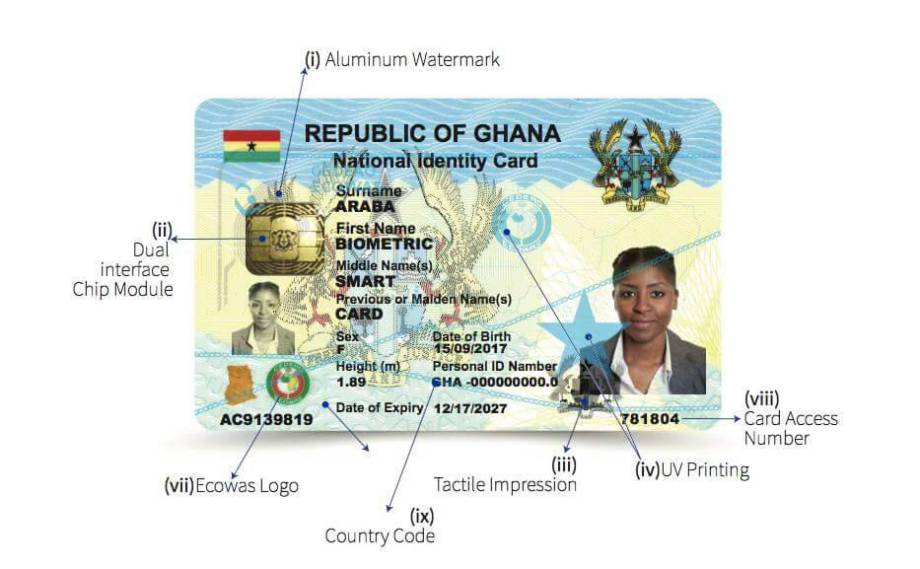

Ghana has spent the better part of a decade building one of Africa’s most ambitious national digital-ID programs. The Ghana Card is biometric, centralized, and backed by a massive enrollment drive that has become a political and logistical benchmark across the continent.

Banks, mobile-money operators, and regulators have long eyed it as the missing link that could slash onboarding costs, fight fraud, and finally bring the unbanked and underbanked into the formal economy.

Yet the gap between vision and operational reality is wide. Integrating a national ID into live payment rails isn’t just a software update. It requires ironclad data-protection rules, real-time verification infrastructure that can handle millions of daily transactions, liability frameworks for when things inevitably go wrong, and—crucially—public trust.

One major breach or privacy scandal could set the entire digital-identity project back years.

For now, Ghanaians will keep using their existing bank cards, mobile-money apps, and the patchwork of fintech solutions that have grown explosively over the past decade. The Ghana Card will remain what it officially is: a powerful proof of identity, not yet a payment instrument.