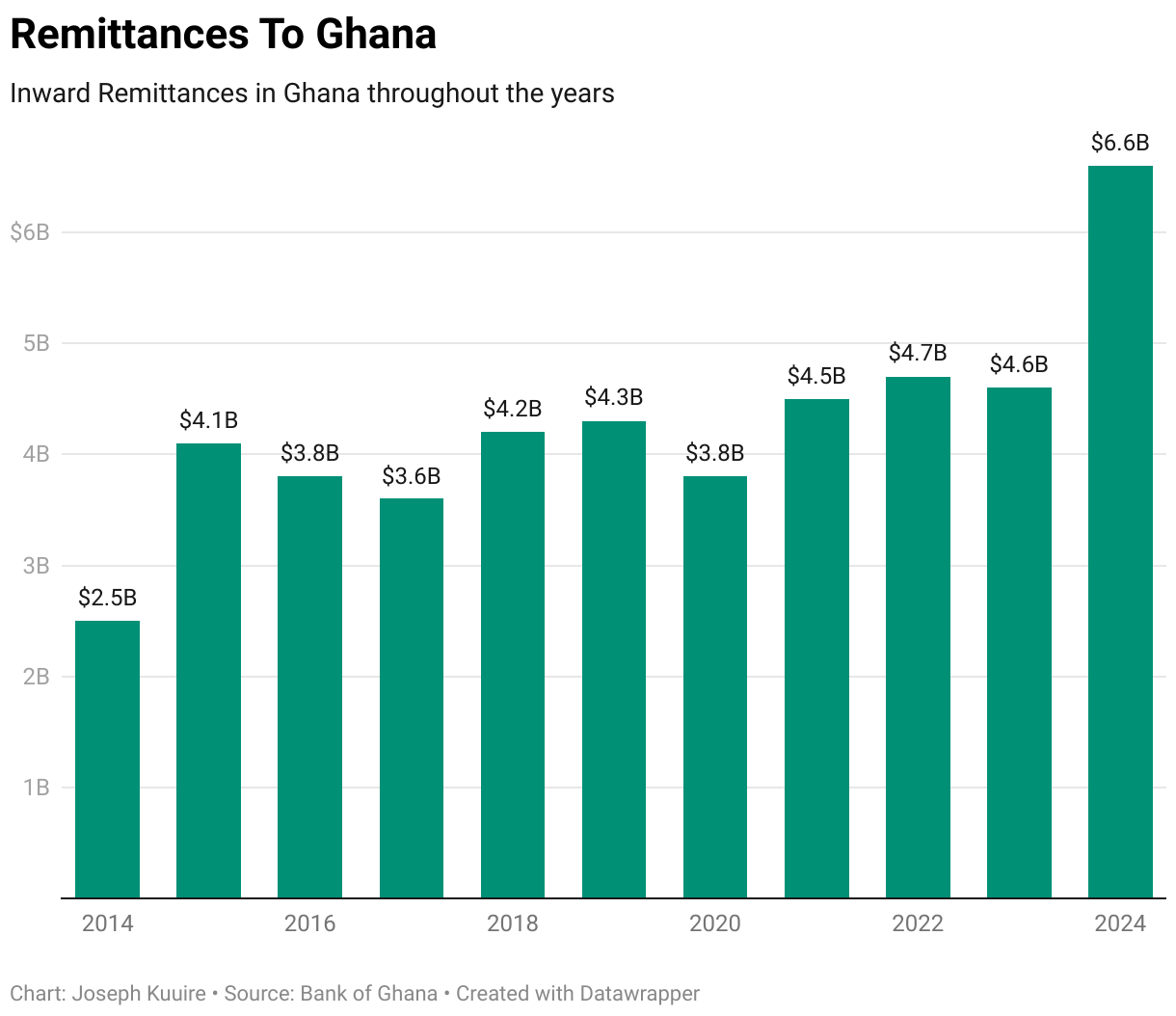

In 2024, Ghana officially recorded $6.65 billion in remittance inflows — and when informal channels are included, the total climbs to an estimated $11.5 billion, nearly a third of the country’s total foreign exchange earnings.

That is more than cocoa. More than gold. It is, increasingly, the financial spine of the Ghanaian economy. And a growing, fast-moving portion of that money is no longer flowing through legacy operators like Western Union or MoneyGram. It’s moving through apps.

The Fee Collapse

The shift is being driven by economics that are almost embarrassingly clear. Traditional remittance fees to Africa have historically ranged from 7 to 12% per transaction. Fintech startups have compressed that to 1 to 3% — and in some cases, to nothing at all. That fee gap isn’t just a convenience.

For a family receiving $300 a month, it’s the difference between $264 and $291 arriving in Accra. Over a year, that’s $324 in recovered income, real money in a country where the median household income remains well under $3,000 annually.

Platforms like LemFi are now handling over $1 billion a month in cross-border transactions, with more than one million active users.

Sendwave, owned by the London-based group Zepz, has become a dominant force specifically in the Ghana-UK and Ghana-US corridors.

Grey, a Nigerian-founded fintech accepted into Y Combinator in 2022, quietly passed one million users by August 2024 and has expanded far beyond West Africa. These are not niche startups anymore. They are infrastructure.

The appeal goes beyond price. The apps connect directly to MTN Mobile Money and Telecel Cash, the mobile wallets that millions of Ghanaians — including those without bank accounts — use daily.

A grandmother in Tamale doesn’t need to travel to a Western Union branch or produce extensive documentation. The money lands in her phone.

| App / Service | Transfer fee | FX markup | Total cost* | Speed | Type | Ghana payout |

|---|---|---|---|---|---|---|

| Fintech — new generation | ||||||

| Sendwave | $0 | 1–2% | ~1–2% | Instant | Mobile-first | MTN, Vodafone Cash, bank |

| LemFi | $0 | 1–2.5% | ~1–2.5% | Instant | Mobile-first | MTN, Vodafone Cash, bank |

| Grey | $0 | 1–2% | ~1–2% | Instant | Multi-currency wallet | Bank deposit |

| NALA | $0 | 1–2% | ~1–2% | Instant | Mobile-first | MTN, Vodafone Cash, bank |

| Remitly | $0–$3.99 | 1.5–2.5% | ~2–4% | Instant–mins | Mobile app | Mobile money, bank |

| WorldRemit | $1.99–$3.99 | 1.5–2.5% | ~3–5% | Minutes | Mobile app | Mobile money, bank, cash |

| Wise | $0.40–$5 | ~0.5% (mid-market) | ~1.5–3% | Minutes–1 day | Multi-currency | Bank deposit only |

| Legacy operators | ||||||

| MoneyGram | From $1.99 | 2–4% | ~4–8% | Minutes | Agent + digital | Cash pickup, bank, mobile |

| Western Union | $1.29–$7.52+ | 2–5% | ~5–12% | Minutes–3 days | Agent + digital | Cash pickup, bank, mobile |

| Ria Money Transfer | Variable | 2–4% | ~3–6% | Minutes | Agent + digital | Cash pickup, bank |

* Total cost = flat fee + FX markup on a $200 transfer. Rates vary by corridor, payment method, and date.

A Policy Headache and a Statistical Anomaly

Ghana’s remittance surge has produced some complicated dynamics for policymakers. World Bank estimates showed Ghana’s remittance inflows surging 91% to $4.6 billion in a single year, making it the fastest-growing recipient on the continent.

But that growth created an unintended problem. As the cedi surged dramatically — gaining over 40% against the dollar — the Bank of Ghana Governor reported a near 50% decline in remittance inflows mid-2025, as diaspora senders paused transfers, re-evaluating the exchange rate math.

It was a reminder that the new digital remittance economy, for all its efficiency, is still exposed to the same macro forces that have always governed cross-border money flows. When the cedi strengthens, the dollars your relatives send buy less. Fintech apps make the transaction faster and cheaper. They can’t fix currency volatility.

By December 2025, though, cumulative remittances had recovered to approximately $7.79 billion for the year, suggesting the disruption was temporary. The long-term trajectory — more volume, more digital, more mobile — remained intact.

What Western Union Is Doing About It

Legacy operators aren’t standing still. Western Union has invested heavily in its digital arm, and now processes a significant share of its global transactions online.

MoneyGram was acquired in 2023 by Madison Dearborn Partners and has aggressively pursued mobile-first partnerships across Africa. Both companies understand the threat. But they carry the legacy costs of global agent networks, compliance teams, and physical infrastructure that newer entrants simply don’t have.

The future of the market is likely to be shaped by accelerating digital transformation, with fintech and blockchain solutions driving lower costs and faster transactions, while mobile money services expand financial inclusion in developing regions.

The Bigger Picture

Remittances to Africa reached an estimated $100 billion in 2024, roughly double the volume of overseas development assistance flowing to the continent — a stat that tends to reframe the entire conversation about foreign aid and development finance.

The diaspora, it turns out, has been running a parallel development program for decades, one that operates without international institutions, donor conferences, or conditionality agreements.

The fintech disruption matters because it routes more of that money to actual households instead of transfer operators. The average cost of sending money through mobile applications to Africa was around 5% in 2023 — still well above the UN’s target of 3% by 2030, but falling steadily as competition intensifies and regulatory frameworks mature.

For a Ghanaian diaspora in the UK, the economics are simple. His family in Ghana gets more money. It arrives faster. And he checks the exchange rate on the same app before he sends. The old way required trust in a global brand. The new way requires trust in a smartphone and a mobile wallet. Increasingly, for millions of Ghanaians abroad, that’s the easier ask.