The value of Mobile Money (MoMo) transactions in Ghana has undergone a breathtaking, multi-trillion Cedi surge, fundamentally reshaping the nation’s financial landscape.

New data from the Bank of Ghana illustrate a decade-long acceleration that cements MoMo’s position as a core engine of the Ghanaian economy.

The Big Picture

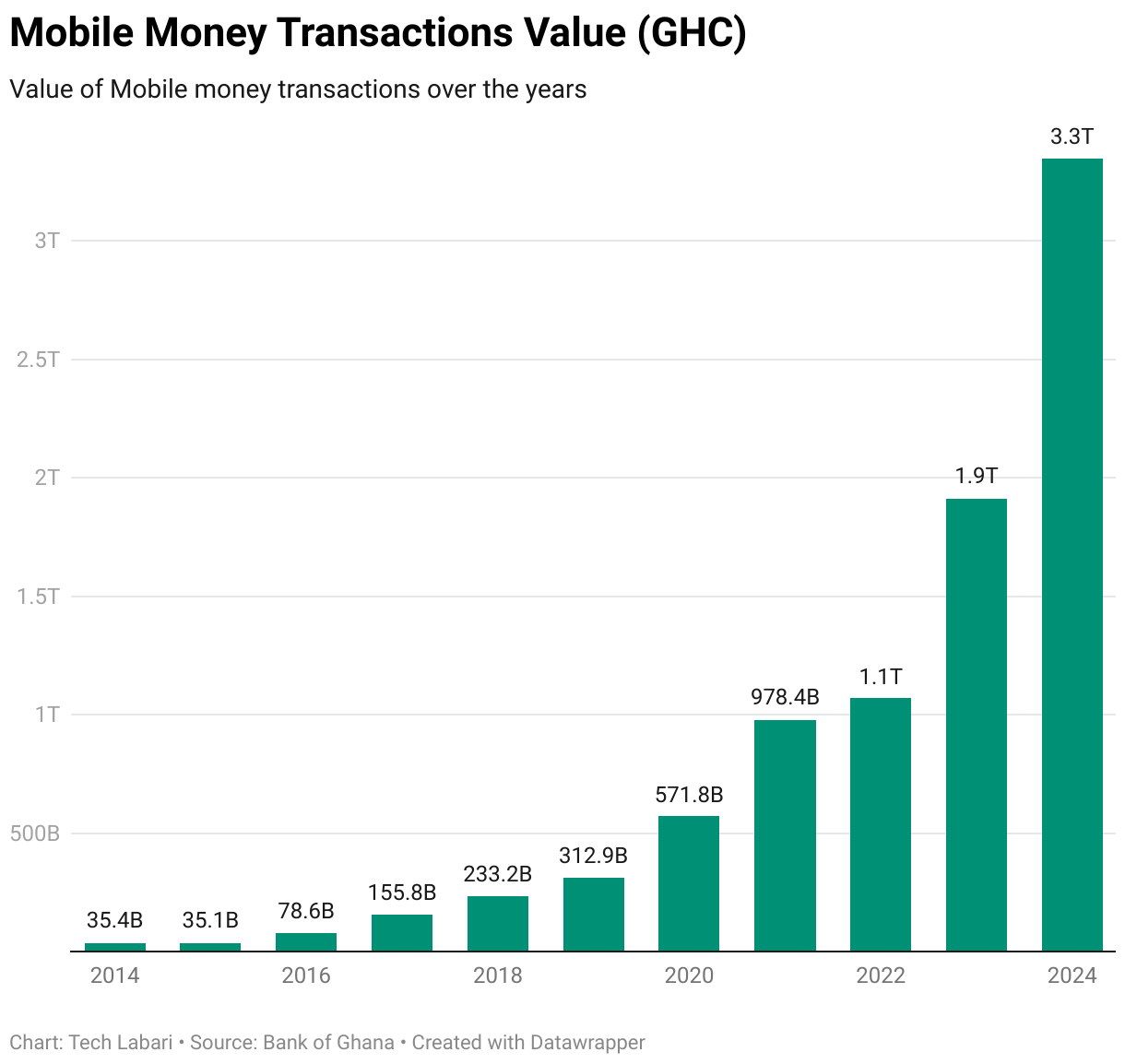

The value of Mobile Money transactions in Ghana soared from just GHC 35.3 billion in 2014 to GHC 3.6 trillion in 2025.

This represents an over 30-fold increase in the value of transactions over ten years.

- 2014: GHC 35.4 billion

- 2024: GHC 3.3 trillion

Why It’s Happening

Several factors converged to fuel this unprecedented growth:

- Financial Inclusion: Ghana has a relatively high mobile phone penetration, but traditional bank branch presence is low, especially in rural areas. MoMo, driven by telecoms companies, became the de-facto mechanism for the unbanked to access basic financial services. It is an accessible alternative to formal banking, requiring only a mobile phone and an ID.

- Regulatory Shift: The Bank of Ghana’s favorable regulatory environment, including the issuance of new guidelines and the push for interoperability (allowing transfers between different MoMo wallets and bank accounts), dramatically improved the ecosystem’s efficiency and user experience.

- Convenience and Use Cases: MoMo transactions expanded well beyond peer-to-peer transfers to include bill payments (utilities, subscriptions), merchant payments, salary disbursements, and even access to micro-credit and savings products. This diversification has deeply embedded the service into the daily economic lives of millions.

- The Agent Network: A vast network of Mobile Money agents, often outnumbering traditional bank branches and ATMs by a large margin, acts as “human ATMs” for cash-in and cash-out transactions, ensuring accessibility even in remote villages.